DigOpp Newsletter - July 2023

Three Charts We Think Are Important

A lot has happened over the month: from court rulings on XRP, to DeFi market structure changes, exploits, and the real world asset narrative chugging along. Here are some things we’re watching.

USDC De-Peg Led to Yield Regime Shift, the Changes to Market Structure Have Been Sticky

In May, we pointed out changes in market structure that arose after the USDC de-peg event in March. These effects have remained sticky and have yet to revert (article below).

USDC's brief de-peg in Q1 (thanks to the Silicon Valley Bank collapse) has reshaped market perceptions. The DeFi lending yield disparity between USDT and USDC has collapsed to zero.

Historically, USDT's greater perceived risk translated to higher yields. However, post the USDC incident, the market seems to have leveled the playing field with the yield spread (difference in lending yield of USDT versus USDC) going to zero and staying there.

Legal Landmarks in Crypto

Earlier this July, the market celebrated as Ripple received a favorable ruling; the judge deemed that XRP tokens sold on exchanges weren't securities.

However, a contrasting statement concerning Terraform Labs threw in a curveball. One judge's stance: where tokens are sold might be irrelevant in classifying them as security sales.

Market impact from regulatory announcements: Bitcoin dominance indicates the share of Bitcoin’s market cap relative to the total market cap of the crypto market. The initial Ripple verdict made Bitcoin's dominance move sharply to the downside on the day of the ruling. Bitcoin has been recognized by the SEC as not being a security, so the market viewed the ruling as a positive for tokens whose status as securities was unclear.

Post the Terraform judge statement? Bitcoin's dominance remained largely unchanged.

However, when zooming out year-to-date, Bitcoin has clearly been in an uptrend relative to the rest of the market.

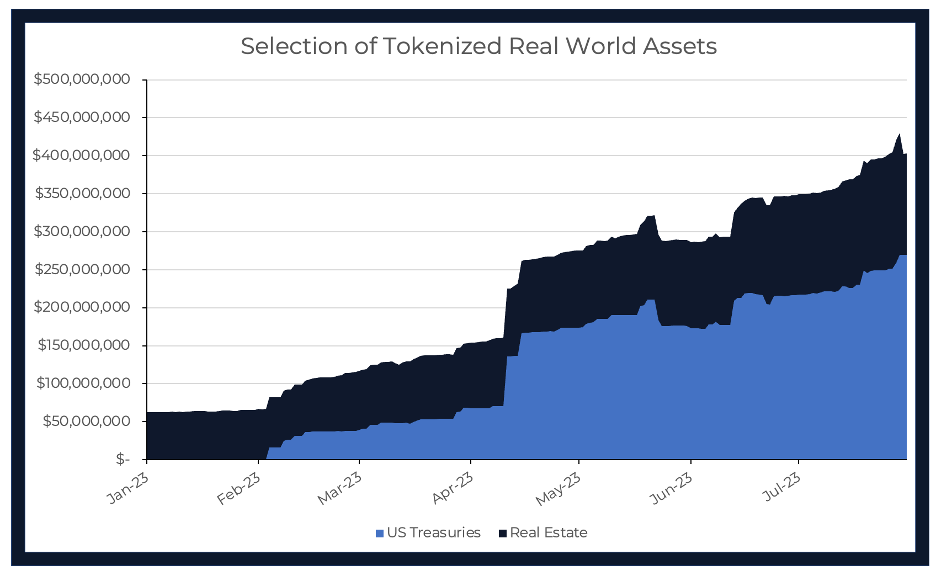

Tokenized Treasuries On the Rise, but Still Relatively Small

Tokenized treasuries could be a real competitor to centralized stablecoins like USDT and USDC. Centralized stablecoin companies back the value of their tokens with assets like treasuries, and pocket the yield as profit.

Now that short dated treasuries offer meaningful returns, these profits are substantial. For reference, Tether, the company behind stablecoin USDT, announced it made more profit than BlackRock. On-chain treasuries would allow those profits to mostly be passed on to the token holders, with potentially the same risk or improved risk profile as fiat-backed stablecoins.

Other tokenized real world assets, like tokenized real estate, have also seen growth.

The below chart shows growth in both tokenized treasuries and real estate. The growth is up and to the right, but it’s not yet very meaningful when compared to the $83 billion and $26 billion market caps of USDT and USDC respectively.

Other important July events:

Curve pool hack and Vyper exploit

Disclaimer

We, Digital Opportunities Group, LLC, are not providing investment or other advice. Nothing that we post on Substack should be construed as personalized investment advice or a recommendation that you buy, sell, or hold any security or other investment or that you pursue any investment style or strategy.

Case studies may be included for informational purposes only and are provided as a general overview of our general investment process. We have compiled our research in good faith and use reasonable efforts to include accurate and up-to-date information. In no event should we be responsible or liable for the correctness of any such research or for any damage or lost opportunities resulting from use of our data.

We are not responsible for the content of any third-party websites and we do not endorse the products, services, or investment recommendations described or offered in third-party social media posts and websites.

Nothing we post on Substack should be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product.