DAO Treasuries: Not Your Grandpa's Institution

DAO treasuries1 are a new breed of institutional investor, existing to support the current and future needs of their parent protocols.

DAO treasuries should frame their asset management approach in a liability aware framework. This means structuring their assets in the context of their spending needs, which have an associated timeframe and risk profile.

However, DAO treasury asset values are exposed to extreme volatility due to high concentration to digital assets (especially their own token, e.g., UNI to the Uniswap treasury), and there are structural reasons which make it difficult to mitigate this volatility. This necessitates unique solutions, purpose-built for DAOs.

DAO treasuries, the cool new institution on the block

Over decades, institutional investors have honed their strategies to manage assets and liabilities. DAO treasuries are the newest breed of these investors, with unique challenges and opportunities.

The objective of this article series is to provide a potential framework that DAO treasuries can utilize to think about managing their portfolio allocations.

In this opening article, we want to set the stage:

What is an institutional investor?

How do institutional investors use their balance sheets to benefit their broader organization?

What similarities and differences do DAO treasuries have with their TradFi counterparts? In particular we look at constraints that DAO treasuries are under, and how these constraints impact their ability to meet their objectives.

A large problem faced by DAO treasuries, which we point out in this article, is that their assets are largely allocated to highly volatile (and often idle) tokens. We want to emphasize here at the outset that these volatile allocations are largely due to constraints from structural market forces, meaning there are substantial difficulties in diversifying these exposures. This point is important, as these causal constraints directly impact the treasury allocation frameworks we will present in future articles.

With this background set, in future articles we will dive deeper into the specifics of frameworks and solutions DAO treasuries can utilize to help ensure sustainability and stability for their protocol and community.

Who are the institutional investors?

There are many kinds of institutional investors: sovereign wealth funds, charitable foundations, family offices, insurance companies, to name a few. Each of these have their own specific investment base (assets) and spending needs (liabilities).

Here we take a look at a few example institutions: university endowments, corporate pensions, and corporate treasuries.

University endowments

University endowments are the pools of assets managed by universities, usually acquired from alumni donations. These assets are used to fund current and future liabilities, such as student aid, faculty positions, research grants, and other operational expenses.

In 1985, David Swensen took over the Yale Endowment and popularized the Yale Model. One of his key understandings was that the liabilities of an endowment are perpetual. This meant the endowment could allocate a large portion of its assets into illiquid investments, like private equity or hedge funds, and generate outsized returns by bearing that illiquidity risk.

Corporate pensions

Where David Swensen revolutionized endowment investing, Rusty Olson did the same to pension investing while at Eastman Kodak. A pension fund is a pool of assets used to pay retirees a payment promised by the parent company. Rusty recognized the importance of diversification and how combining multiple return streams together helps to reduce the burden on the parent company. This diversification helps reduce the correlation of the pension assets to the performance of the parent company.

If the pension fund was invested in assets highly correlated to the performance of the parent company, and if the parent incurred significant losses during a market downturn, it may require the parent to contribute money to the fund. This would put further strain on the parent company as they have to contribute funds to the pension when they are already in a period of financial stress.

Corporate treasuries

Another type of institution is a corporate treasury. A corporate treasury seeks to manage the company’s cash to meet short term needs (like payroll, or dividends) and long term needs (like long term investments, long term debts). They also seek to to help minimize risks the company may be exposed to, like interest rate risk (from their bonds they’ve issued), or commodity risk (an airline company may trade jet fuel futures to lock in their fuel cost).

While corporate treasuries are not typically considered an institutional investor, we think it is useful to include them here. The reason for this is that DAO treasuries resemble a very interesting mix of a few institutional types. Depending on which way you look at the DAO treasury, they may look like an endowment (research grants), a corporate treasury (short term cash needs, token buybacks), or a pension (volatility of assets and liabilities, while considering correlation between the two).

Harmonizing the balance sheet

What is a commonality shared across each of these institutions? Over time, these institutions have developed liability aware investment frameworks. To put it another way, they are looking for ways to harmonize their assets and liabilities:

The endowment has a perpetual time horizon, with the objective to last forever and pay out a small amount each year. This makes long term, illiquid investments a good fit.

The corporate pension must pay back pensioners who have a certain expected life span. So the pension invests in a diversified allocation of assets, and bonds with maturities similar to the expected life of the pensioners.

A corporate treasury uses their cash to allocate to instruments like interest rate swaps to hedge the interest rate risk of the corporate’s issued bonds, or futures to hedge commodity related costs.

The table below summarizes these institutions, and includes the average DAO treasury:

The pie chart below shows the breakdown of assets within the average treasury:

You can see that the majority of the holdings are in the treasuries' “associated protocol token” (i.e., UNI tokens in the Uniswap Treasury). The allocation to assets excluding stablecoins is over three quarters of the exposure.

Due to market forces that have, until recently (as we will show in upcoming articles), been largely out of the control of DAO treasurers, the value of treasuries have largely been exposed to extreme levels of volatility due to digital asset positions dominating their holdings.

What if Rusty Olson invested a large portion of the Kodak pension in Kodak stock?

What if the Kodak company then began to struggle, and generate less cash? Most likely, their stock price would decline. Now the value of the pension would suffer at the same time as the parent company.

In that case the Kodak parent company would be forced to contribute cash to the pension right at the worst possible time. The risk from the investments spills over into the company itself!

Sushiswap’s conundrum

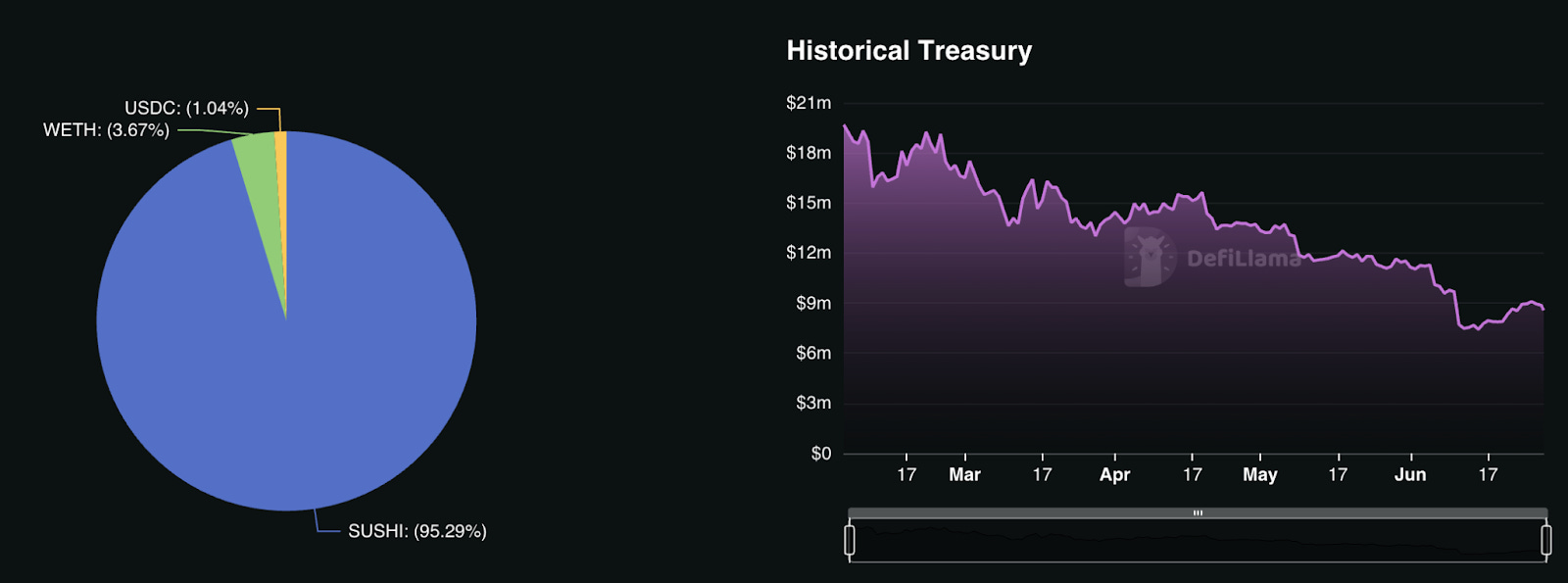

An example of this concentration risk, spilling over as a risk to the protocol itself can be found with Sushiswap.

The Sushiswap treasury is and has been almost entirely allocated to their native token, SUSHI.

The extreme volatility of the recent digital asset market placed massive pressure on the Sushiswap treasury, putting them in the difficult position to take drastic measures. In a forum post in December 2022, the head of Sushiswap outlined the problems they were facing, stating that they only had 1.5 years of runway.

This forced Sushiswap to direct a significant portion of protocol revenue away from SUSHI stakers and directly into the Sushiswap treasury. The proposal passed early this year.

This proposal clearly had an impact on the market’s perception of SUSHI. Redirecting revenues away from stakers to the treasury negatively impacts the utility of SUSHI itself.

Below we show the performance of SUSHI compared to UNI, a comparable token as Sushiswap began as a fork of Uniswap. The performance begins in December of 2022, when the proposal was initially made. You can see SUSHI has substantially underperformed over this time period.

If tokens are so volatile, why don’t treasuries just sell them? Because of market forces.

Given these examples, the reader’s first thoughts may be to criticize these treasuries for being so concentrated. However, it is not that simple. There are powerful structural forces which make it difficult for treasuries to diversify their exposure:

Treasuries are usually major holders of a token. Liquidating treasury assets can have significant negative market impact.

There is a lack of community support for the treasury to sell tokens. Community members may also desire the treasury to remain aligned with the performance of the protocol, which is likely correlated with the token value (“don’t rug me!”).

Aside from the market impacts of token sales, a treasury selling tokens can also be a negative signal to broader participants.

Where do we go from here?

In this article we have given a general background on how various institutions utilize their portfolios to help meet the needs of their parent organization. We have also covered how DAO treasuries compare to institutions more broadly, and the constraints treasuries find themselves in to help their parent protocol’s ensure sustainability and stability for years to come.

Given this background, over the next few articles we will explore a flexible framework for DAOs to think about managing their assets.

About DigOpp

We are a specialty finance firm focused on bridging the gap between traditional and decentralized markets.

Our protocol solutions include liquidity vehicles that generate protocol-owned-liquidity and put idle assets to work, liquidity incentive analysis, portfolio construction, hedging strategies, and advisory services. If you have a unique need, we love building creative solutions.

For traditional investors, we offer unique, systematic hedge fund strategies focused on digital assets in both CeFi and DeFi.

For further inquiries, please reach out at info@digopp.group

Disclaimer

We, Digital Opportunities Group, LLC, are not providing investment or other advice. Nothing that we post on Substack should be construed as personalized investment advice or a recommendation that you buy, sell, or hold any security or other investment or that you pursue any investment style or strategy.

Case studies may be included for informational purposes only and are provided as a general overview of our general investment process. We have compiled our research in good faith and use reasonable efforts to include accurate and up-to-date information. In no event should we be responsible or liable for the correctness of any such research or for any damage or lost opportunities resulting from use of our data.

We are not responsible for the content of any third-party websites and we do not endorse the products, services, or investment recommendations described or offered in third-party social media posts and websites.

Nothing we post on Substack should be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product.

Using the term “protocol treasury” is likely more accurate than DAO treasury. Not all treasuries associated with a protocol are managed by, or even associated with a DAO. The industry seems to be familiar with the term DAO treasury, so we go with that in this article.